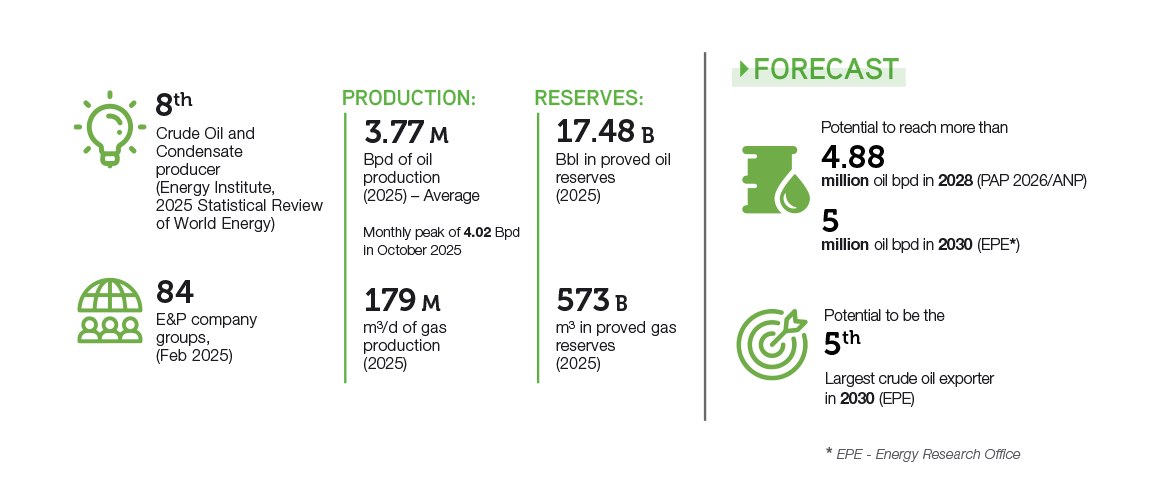

Investment Opportunities in Brazil

- Highlights 2026

Free digital technical data

- Concession and Production-Sharing Regimes

The discovery of the Pre-salt Polygon in 2007 led the Brazilian government to establish the Production-Sharing Regime in 2010. Before that, all areas were under a Concession Regime. Since then, Brazil has operated with a mixed regulatory regime.

How the Concession Regime Works

Under the Concession Regime, the concessionaire assumes the risk of investing to discover oil or natural gas. It will then have ownership of any oil and gas discovered in the concession area.

In the bidding rounds, the company or consortium that submits the most advantageous bid, in accordance with the terms of the tender protocol, is awarded the right to explore the area to verify the existence of oil or natural gas deposits.

On that occasion, interested companies or consortia offer an amount for the signature bonus and propose a Minimum Work Program (PEM). This program details the activities, such as seismic surveys and well drilling, that the concessionaire commits to carrying out in the concession area.

Under a concession contract, the concessionaire shall pay various government-take components, such as the signature bonus, royalties, annual acreage fees for onshore blocks, and a special participation for fields that produce large volumes.

The Brazilian National Agency of Petroleum, Natural Gas and Biofuels (ANP) signs these contracts on behalf of the Union – the federal entity of Brazil, which has its own legal personality, collects taxes, owns property, and represents the country abroad.

How the Production-Sharing Agreement Works

For areas in the Pre-Salt Polygon and other strategic areas, the Brazilian National Council for Energy Policy (CNPE) decides whether to hold bidding rounds or directly contract Petrobras. The objective is to safeguard national interests and meet energy policy goals. In both situations, contracts are signed under the production-sharing regime.

If the CNPE decides to hold a bidding round, Petrobras has the preferential right to operate the blocks. If Petrobras chooses to exercise this right, it must indicate the areas of interest and its participation in the consortium, which must be at least 30%.

The CNPE defines the blocks and the technical and economic parameters of the production-sharing agreement, while the ANP organizes the bidding round. The Ministry of Mines and Energy (MME) sets the guidelines for ANP to follow when preparing the bidding documents and contracts, which are later approved by the ministry.

In production-sharing bidding rounds, the winner is the one offering the Brazilian State the largest share of oil and natural gas, that is, the largest portion of exceeding oil.

The consortia exploring a pre-salt area are necessarily composed of a state-owned enterprise, Pré-Sal Petróleo S.A. (PPSA), representing the Union, and the winning companies. The contracts are signed by the MME on behalf of the Union.

- How to contract areas for exploration and production in Brazil

In Brazil, there are two ways to contract areas for oil and natural gas exploration and production: bidding or farm-in.

Bidding

It is the tender process in which companies submit formal proposals and bids to acquire rights to an area for oil and gas exploration. This process can occur through:

- Traditional Bidding Rounds – The government publishes a notice with the rules, the evaluation criteria, and the areas on offer. Companies then have a set period to study the areas before submitting bids in a public session. It is applied both to concession and production-sharing agreements.

- Open Acreage System – It is a continuous bidding process that allows companies to express interest in and bid on available exploration blocks throughout the year. Companies from anywhere in the world may also suggest new areas, subject to ANP’s review and approval. It contrasts with traditional Bidding Rounds, which have specific calendar dates. The system covers both onshore and offshore areas, including the pre-salt polygon. This is now the main model used in Brazil. Read more about Open Acreage in the next section.

Explore opportunities and updates at Rounds ANP.

Farm-in

It is a commercial agreement whereby a company or consortium acquires a partial working interest in an exploration concession or block from another company or consortium, which is the original rights holder. In simple terms, it represents the entry of a new partner into an oil exploration or production project.

- Open Acreage

Since CNPE Resolution No. 27/2021 took effect in December 2021, the Open Acreage system has been the main model for conducting tenders for new oil and gas exploration areas. This system operates under two distinct modalities:

- Production-Sharing Open Acreage (OPP), for strategic areas and the Pre-salt Polygon; and

- Concession Open Acreage (OPC), for all other areas.

Nomination of areas by economic agents

The ANP Resolution No. 837/2021 is a key regulation for the nomination of areas by oil and gas companies from anywhere in the world. This resolution creates a process for the market to suggest new areas of interest for the Open Acreage.

Additionally, it allows companies to change the design of existing blocks to better match identified prospects, leads, or even clusters of structures, making these areas more attractive.

Outcome of the Open Acreage O&G Bidding Rounds

Reference exchange of the comercial U.S. dollar (PTAX - Central Bank of Brazil) on April 15, 2026: BRL 4.99 USD)Concession: Five cycles; 340 exploratory blocks and areas awarded; BRL 4.33 billion (≈ USD 870 million) in minimum investment and BRL 1.909 million (≈ USD 383 million) in signature bonuses.

Production Sharing: Three cycles; ten exploratory blocks awarded; BRL 1.91 billion (≈ USD 450 million) in minimum investment and BRL 1.70 billion (≈ USD 206 million) in signature bonuses.

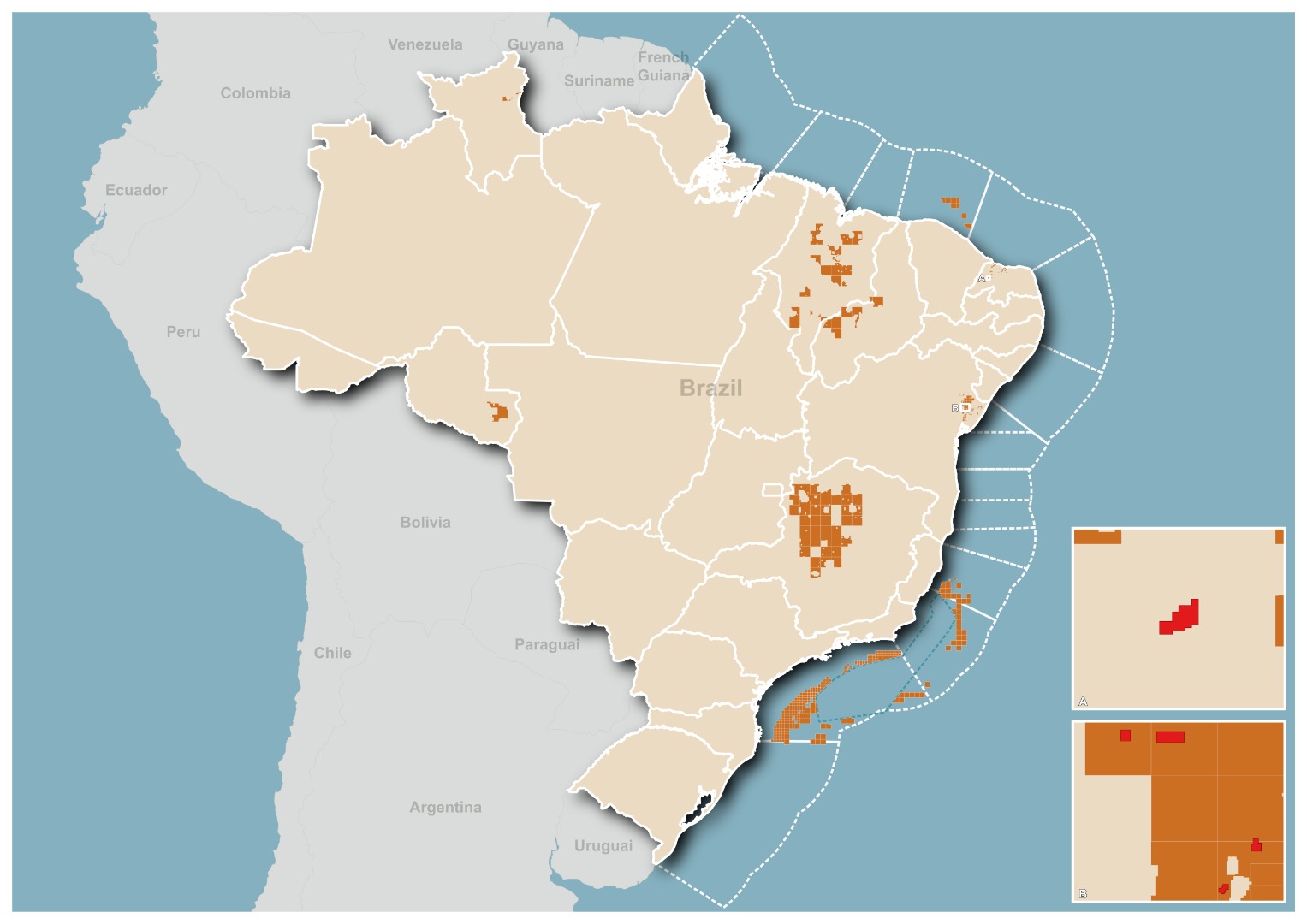

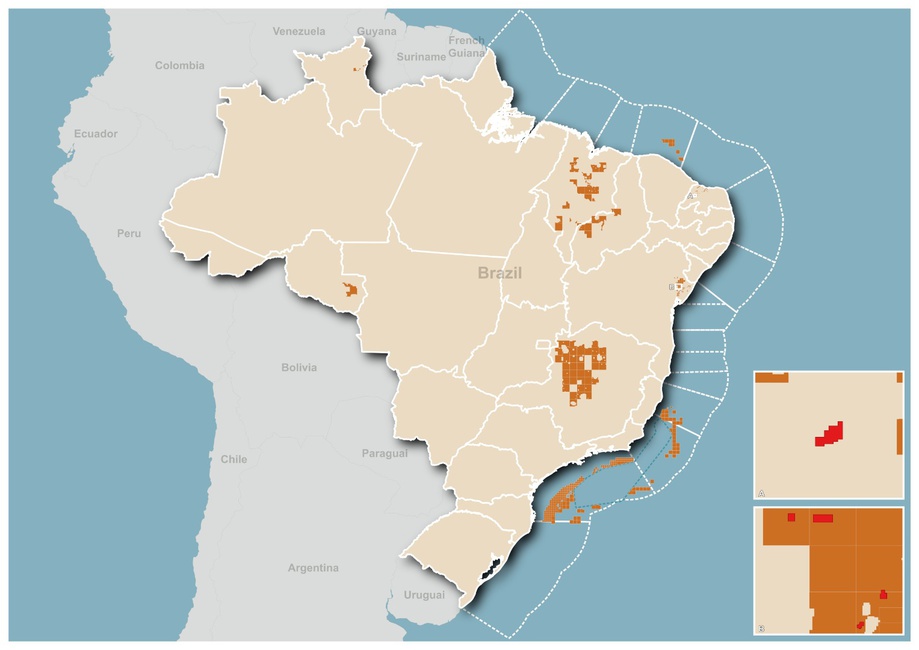

Opportunities in the Open Acreage

As of April 2026, 450 exploration blocks (onshore - 174 and offshore - 276) and 5 marginal oil accumulation fields are available through the Open Acreage of Concession (OPC). And 45 blocks are under inclusion process - publication of Tender Protocol in May.

In addition, 1,523 blocks are being evaluated, along with 4 marginal oil accumulation fields, for possible inclusion in the OPC in the future.

- OPC

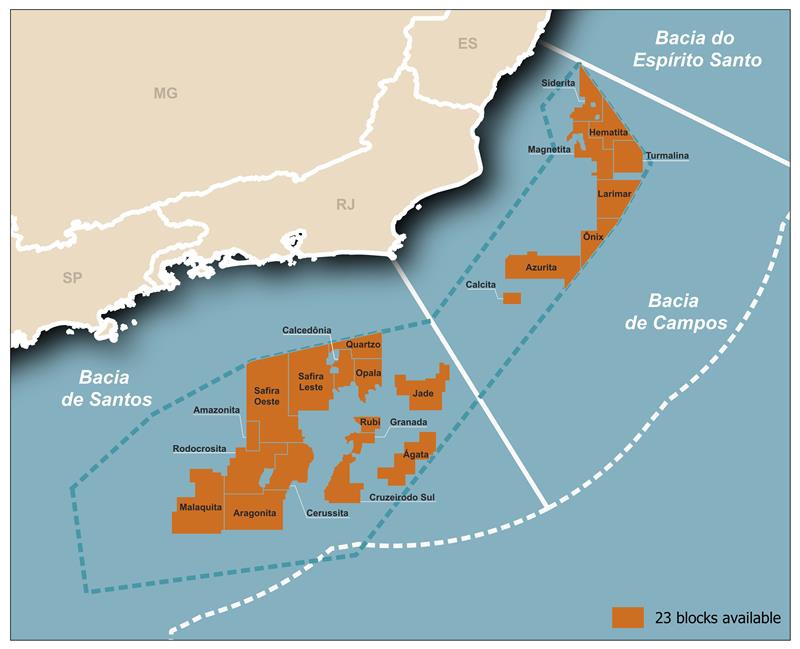

And 23 areas in the Pre-Salt are available through the Open Acreage of Production Sharing (OPP). Additionally, 3 blocks are being evaluated for possible inclusion in the OPP in the future.

- OPP

Explore opportunities and updates at Rounds ANP.

- E&P Strategic Goals and Measures

-

A Competitive and Stable Upstream Environment

Brazil offers one of the most dynamic and attractive environments for oil and gas exploration and production globally. The country combines strong geological potential, a stable regulatory framework and a diversified industry structure, creating long-term opportunities for investors across multiple business models.

Stable Regulatory Framework

Brazil’s upstream sector operates under a stable, transparent and predictable regulatory system, implemented by the ANP.

Since the opening of the sector to competition in the late 1990s, Brazil has built a regulatory framework that provides:

- Legal certainty for long-term investments

- Clear contractual regimes, including concession and production sharing

- Equal conditions for domestic and international companies

- Regular licensing rounds and transparent procedures

This stable regulatory environment has enabled Brazil to attract consistent investment from a wide range of global and independent operators.

A Diversified Upstream Industry

Brazil has developed a highly diversified ecosystem of oil and gas operators.

Today, more than 50 companies operate producing oil and gas fields in Brazil, reflecting the maturity and openness of the Brazilian upstream sector. The number of operators has grown significantly since the early years following market liberalization.

This diversity includes:

- Major international oil companies

- Brazilian operators

- Independent companies specializing in mature fields and onshore production

A diversified operator base contributes to greater competition, technological innovation and the development of local supply chains.

Three Complementary E&P Environments

Brazil offers investment opportunities across three distinct exploration and production environments, each with specific geological characteristics and business opportunities.

Onshore Opportunities

Brazil’s onshore basins provide attractive opportunities particularly for independent and medium-sized companies, including mature field revitalization and new exploration plays.

Onshore production also plays an important role in regional economic development, with activity concentrated in basins such as Potiguar, Recôncavo and Sergipe-Alagoas.

Conventional Offshore Basins

Brazil’s offshore basins are among the most productive petroleum provinces in the world.

Areas such as the Campos, Santos and Espírito Santo basins offer opportunities ranging from mature field redevelopment to new deepwater exploration projects.

The Pre-Salt Province

The Brazilian pre-salt province is one of the most important petroleum discoveries of the 21st century and represents the backbone of Brazil’s oil and gas production.

Pre-salt reservoirs account for the majority of national production and continue to attract major global investments due to their high productivity and world-class resource potential.

Long-Term Opportunities for Investors

Brazil’s upstream sector combines:

- Stable regulation

- Diverse geological opportunities

- A competitive and open market

- A wide range of operators and investment models

Together, these elements position Brazil as one of the most promising destinations for long-term oil and gas investment.

Local Content

Brazil’s local content policy seeks to strengthen the domestic supply chain for the oil and natural gas industry while maintaining a competitive environment for upstream investments.

Local content commitments are defined in exploration and production contracts awarded in licensing rounds. The National Agency for Petroleum, Natural Gas and Biofuels (ANP) is responsible for regulating, implementing and monitoring compliance with these contractual requirements.

Recent regulatory improvements have increased flexibility in the implementation of the local content policy.

Lei nº 15.075/2024 introduced mechanisms that allow companies to transfer certified local content surpluses between exploration and production contracts, improving efficiency in meeting contractual commitments while preserving the objective of strengthening Brazil’s oil and gas supply chain.

Decommissioning Opportunities

Brazil is entering a new phase in its oil and gas lifecycle, with a growing portfolio of decommissioning projects that create significant opportunities for specialized service providers, engineering companies, and the offshore supply chain.

According to projections based on operators’ investment plans, approximately R$70 billion (around US$13 billion) are expected to be invested in decommissioning activities between 2025 and 2029 in Brazil’s upstream sector.

These activities include a wide range of technical operations such as:

- permanent well abandonment

- removal of subsea pipelines and equipment

- platform decommissioning and dismantling

- site clearance and environmental restoration

-

- Natural Gas opportunities

- Natural gas as a strategic energy source: Brazil recognizes natural gas as a key pillar for economic development and the energy transition, supporting reliable energy supply, enhancing industrial competitiveness and contributing to a lower-carbon energy system.

- Advancing Brazil’s New Gas Market: The implementation of the New Gas Law is transforming the sector into a more open and competitive market, with expanded third-party access to infrastructure, increasing participation of new suppliers and shippers, and more flexible commercial arrangements in the wholesale gas market.

- Modernized transportation tariff framework: Brazil has updated its natural gas transportation tariff regime in line with international best practices, strengthening transparency, regulatory certainty and long-term investment signals across the gas value chain.

- Ongoing regulatory improvements: Further regulatory advancements are expected in 2026, including updates to the regulatory framework governing the construction, expansion and operation of midstream infrastructure, as well as improvements to third-party access rules for essential gas infrastructure, including LNG terminals and dispute resolution mechanisms.

- Natural gas as a strategic energy source: Brazil recognizes natural gas as a key pillar for economic development and the energy transition, supporting reliable energy supply, enhancing industrial competitiveness and contributing to a lower-carbon energy system.

- Downstream opportunities

- One of the world’s largest fuel markets: Brazil offers a large and dynamic fuel market supported by a nationwide logistics and distribution network, creating significant opportunities across refining, fuel distribution, retail and supply infrastructure.

- Modern regulatory framework for fuel supply: Continuous regulatory improvements – including updated rules for imported fuels – strengthen market transparency, ensure fuel quality and facilitate integration with global fuel markets.

- Global leader in biofuels: Brazil’s well-established biofuels industry and ambitious blending policies continue to expand opportunities in the production, logistics and commercialization of sustainable fuels.

- Robust market governance: Strong regulatory oversight, advanced monitoring technologies and coordinated enforcement actions help ensure market integrity, fair competition and a stable environment for long-term investment.

- One of the world’s largest fuel markets: Brazil offers a large and dynamic fuel market supported by a nationwide logistics and distribution network, creating significant opportunities across refining, fuel distribution, retail and supply infrastructure.

- Decarbonization and Energy Transition

- Brazil is one of the most attractive emerging markets for renewable energy investments: The country is the second-largest producer of biofuels in the world, behind only the United States. Biofuels play a central role in the transport sector: around 30% of the energy used in road transport comes from renewable fuels, and more than 80% of the light-duty vehicle fleet is flex-fuel, capable of running on gasoline and ethanol.

- RenovaBio Program: Since the beginning of the National Biofuels Policy, more than 206 million tons of CO2 equivalent have been avoided; the program aims to expand the production and use of biofuels in Brazil.

- Fuel of the Future initiative: Brazil is advancing a comprehensive policy framework to accelerate the deployment of low-carbon fuels, creating new investment opportunities in sustainable aviation fuel (SAF), renewable diesel and biomethane.

- Emerging biomethane market: Regulatory initiatives supporting certification and guarantees of origin are enabling the development of biomethane market and new opportunities for gas decarbonization.

- Hydrogen market development: Brazil is advancing regulatory initiatives to support the development of a low-carbon hydrogen market, providing guidance for project authorization and encouraging early-stage investments.

- CCS and BECCS: The development of regulatory frameworks for CCS is opening new opportunities for emissions management and large-scale decarbonization. Brazil also offers strong potential for bioenergy with carbon capture and storage (BECCS), leveraging its large biofuels and biomass industries to support the development of negative-emissions solutions.

- Innovation-driven energy transition: Brazil benefits from a strong innovation ecosystem supported by significant annual investments in research, development and innovation through ANP’s mandatory R&D clause in oil and gas contracts.

- Transparency in emissions management: Expanded public data and reporting initiatives on greenhouse gas emissions enhance transparency and support industry strategies toward net-zero goals.

- Brazil is one of the most attractive emerging markets for renewable energy investments: The country is the second-largest producer of biofuels in the world, behind only the United States. Biofuels play a central role in the transport sector: around 30% of the energy used in road transport comes from renewable fuels, and more than 80% of the light-duty vehicle fleet is flex-fuel, capable of running on gasoline and ethanol.